Wholesale Price Index (WPI) Movement of Cotton Value Chain in India: Diverging Price Trends in Q1 2026

- By Nabarun Kar, a technocrat with nearly 30 years of cross‑industry experience spanning Production, Strategy & Planning, Marketing, Business Development, and Policy Advocacy at leading organisations. His career reflects a consistent ability to drive operational excellence, shape strategic direction, and influence policy frameworks, while building strong stakeholder relationships and delivering sustainable growth

- May 15, 2026

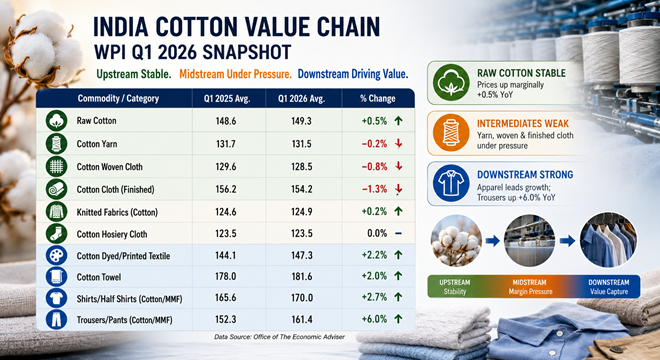

The first quarter of 2026 has revealed a nuanced picture of India’s cotton value chain, as reflected in the Wholesale Price Index (WPI). While raw cotton prices showed only a marginal uptick, downstream apparel categories registered stronger gains, highlighting a shift in value capture along the textile chain. Cotton Value Chain – WPI Q1 Comparison

| Commodity / Category | Q1 2025 Avg. | Q1 2026 Avg. | % Change |

| Raw Cotton | 148.6 | 149.3 | +0.5% |

| Cotton Yarn | 131.7 | 131.5 | –0.2% |

| Cotton Woven Cloth | 129.6 | 128.5 | –0.8% |

| Cotton Cloth (Finished) | 156.2 | 154.2 | –1.3% |

| Knitted Fabrics (Cotton) | 124.6 | 124.9 | +0.2% |

| Cotton Hosiery Cloth | 123.5 | 123.5 | 0.0% |

| Cotton Dyed/Printed Textile | 144.1 | 147.3 | +2.2% |

| Cotton Towel | 178.0 | 181.6 | +2.0% |

| Shirts/Half Shirts (Cotton/MMF) | 165.6 | 170.0 | +2.7% |

| Trousers/Pants (Cotton/MMF) | 152.3 | 161.4 | +6.0% |

Raw Cotton: Stability Amid Softness

Raw cotton prices averaged 149.3 in Q1 2026, a modest 0.5% increase over the previous year. This stability suggests that raw fibre markets are balancing supply-side pressures with steady demand, but without significant upward momentum.

Intermediates: Weakness Persists

Cotton yarn and woven cloth continued to exhibit softness. Yarn slipped 0.2%, woven cloth declined 0.8%, and finished cloth fell 1.3% compared to Q1 2025. These declines underscore the persistent margin squeeze in intermediate processing, where competitive pressures and subdued demand weigh heavily.

Knitted & Hosiery: Holding Ground

Knitted fabrics of cotton edged up 0.2%, while hosiery cloth remained flat. This resilience indicates niche demand stability, though without strong growth impulses.

Value-Added Textiles: Signs of Recovery

Dyed and printed textiles rose 2.2%, and cotton towels gained 2.0%, reflecting renewed consumer demand for finished textile products. These categories benefited from both domestic consumption and export traction.

Apparel: Strong Downstream Momentum

The standout performers were apparel categories blending cotton and man-made fibres. Shirts rose 2.7%, while trousers surged 6.0%, marking the strongest growth across the value chain. This divergence highlights how downstream apparel is capturing value even as raw and intermediate segments stagnate.

Strategic Implications

The Q1 2026 WPI data reinforces a critical narrative: value is migrating downstream. Raw cotton and yarn remain under pressure, but apparel categories are consolidating gains, driven by consumer demand and product differentiation. For industry stakeholders, this signals the need to reorient strategies toward finished goods and blended fabrics, where pricing power and margins are stronger.

In essence, the cotton value chain is experiencing a decoupling—with upstream stability, midstream weakness, and downstream strength. This dynamic will shape trade flows, investment priorities, and policy debates in the textile sector through 2026.

Data Source: Office of The Economic Adviser

The Q1 2026 WPI data reinforces a critical narrative: value is migrating downstream. Raw cotton and yarn remain under pressure, but apparel categories are consolidating gains, driven by consumer demand and product differentiation. For industry stakeholders, this signals the need to reorient strategies toward finished goods and blended fabrics, where pricing power and margins are stronger. In essence, the cotton value chain is experiencing a decoupling—with upstream stability, midstream weakness, and downstream strength. This dynamic will shape trade flows, investment priorities, and policy debates in the textile sector through 2026.

Subscribe To Textile Excellence Print Edition

If you wish to Subscribe to Textile Excellence Print Edition, kindly fill in the below form and we shall get back to you with details.

...

Newsletter

Subscribe To Textile Excellence Mailing List

2...

- December 09, 2022

'There Is Very High Acceptance For India

- December 09, 2022

'Advanced Machines & Service, Customer C

- October 09, 2023

First-time In The World: Rieter’s Auto

- October 31, 2023

Denge & Dyesol India: Leading The Way In

- June 01, 2020

Karl Mayer Enables Automated Production

- June 05, 2023

Ultimax - All New Revolutionary Rapier W

- June 09, 2025